Well…they’re kind of offering a bank product

I have been a long time user of Vanguard and will still use Robinhood for my spreads and real time data for stock options. For as long as I can remember using Robinhood, they’ve offered an interest amount (pretty low at the time of wring of 1.5%) on your cash in their account. If you purchase Robinhood Gold you can pull in 5% APY (5.25% bonus right now). To be honest, that seemed pretty enticing until I realized I had to pay for Gold at $5 a month and that just chewed up too much of that return. Especially when I don’t keep cash in the brokerage settlement fund for too long.

I transfer cash in from my High Yield Accounts earning 5% already then buy the stocks I want. With Vanguard, I just left it in the Money Market they had, which had a yield of about 5.5% at the time of writing. I woke up to an email from them just last week though that said they have a new option for the settlement fund that just happened to be an FDIC insured bank product (as they stated). That was pretty exciting for me until I gave them a call and took a look at the disclaimers.

Vanguard took a note from a competitor

Vanguard is pretty big. They’ve been around for a long time, but Robinhood has really rattled their cage (along with other brokerage apps like Webull and Alinea-Invest). They have taken a lot of the new aspiring investors by making it easier to understand and create a platform based on those new investors feedback. Vanguard never had a bank option (or at least in the years I’ve been investing with them) and now they just launched it PROBABLY due to the greater competition in the market. I was excited because I could maybe make a bit more off the interest. I was actually a bit disappointed when I saw the rate and the end result. I read the note at the bottom of the Vanguard email and it should have given me all the information I needed.

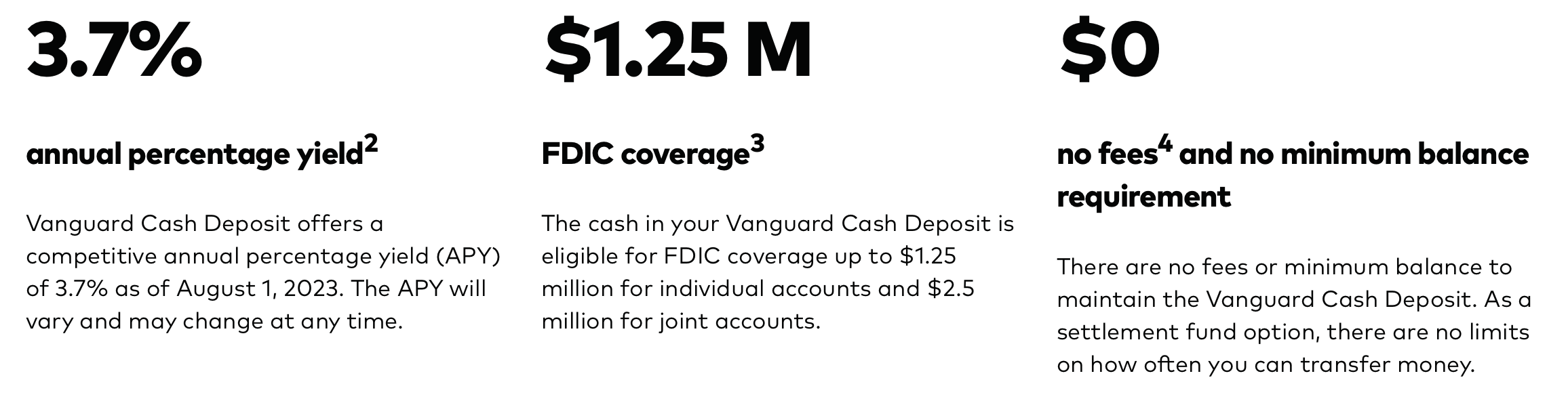

You now have another option to preserve value in your brokerage account. Vanguard Federal Money Market Fund is a mutual fund, while Vanguard Cash Deposit is a bank product. Both options aim to preserve capital, but they may perform differently depending on the interest rate environment.

What I’m doing with this news

After digging a little deeper and finding that the APY is lower than almost EVERY High Yield Bank Account out there AND it’s lower overall yield compared to the money market. I also called in to the customer service line just to confirm the major difference (besides one being a bank product). The answer?! Really just the amount of insurance (The FDIC insurance is up to $1.2 Million). Sorry but if you’re playing around with $1.2 Million you’re probably not lobbing it into a Vanguard Cash Account pulling 3.7% APY.

I’ve also got to keep in mind what is happening in the economy with inflation still pretty high and interest rates not coming down any time soon. While that’s bad for the value of the dollar, that’s good for High Yield Bank Accounts.

SO… I will continue to allow my ETFs to reinvest as the market goes down and I will transfer additional cash in when I want to purchase more. This let’s me continue to pull in the 5% through my High Yield Bank accounts. As for Vanguard, I’ll be leaving my settlement fund with the Money Market Mutual Fund. I have to say Vanguard did a good job with the marketing campaign and got me to click the link – they caught my attention. I’m sure they got a lot of other people too because it’s tough out there right now. People are looking for ways to make more money and preserve wealth. While I won’t be changing my settlement fund it was a good reminder in always doing some research before changing things.