Marty McFly would be proud

Well we haven’t actually figured out time-travel. Sorry everyone – I’ll let you know when we do since I’ll be going back in time to buy Bitcoin at a $1. Home buyers are just looking into something called an assumable mortgage and now even real estate agents, real estate companies like realtor.com, and your friendly local resource biggerpockets.com are all talking about it. Why? Because you can basically go back in time and ‘assume’ the old mortgage and more importantly the RATE!

What’s the catch?

You know there is always something that makes a sweet deal not so sweet. Surprisingly, an assumable mortgage doesn’t have too many ‘catches,’ but there are a few to be aware of. To kick things off what is this?

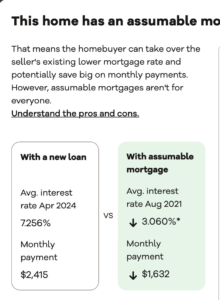

An assumable mortgage allows a buyer to assume the rate, repayment period, current principal balance and other terms of the seller’s existing mortgage.

Sounds like a pretty good deal for the buyer really, but everyone has some pros and cons.

For the buyer

Pros:

– As a buyer you get to assume a lower rate. We’re talking hundreds of dollars difference a month.

– Fewer upfront costs since there isn’t an origination of a loan.

– Longer term savings because you’re paying less in interest over the years especially if you take the loan to term.

Cons:

– Few to choose from since the mortgage must be FHA, VA, or USDA. Some conventional loans are assumable, but you have to check your contract, with your lender, and talk with your attorney.

– The buyer has to make up the difference between the remaining loan balance and equity in the home. That can be either a downpayment in cash or a second loan at todays interest rates. Example would be the home is worth $400,000 and the remaining balance is $250,000. That means the buyer has to come up with $150,000.

– Must use the same lender the buyer originally used since the buyer is ‘assuming’ the mortgage.

– Lenders take longer typically.

For the seller

Pros:

– You get to offer the home at a ‘lower’ rate to prospective buyers in a sellers market.

Cons:

– As the seller, if the buyer defaults the seller can be held liable but that’s all contractual stuff pending the loan.

– Lenders sometimes take a bit more time.

– Less buyers are qualified typically.

For the lender

Pros:

– The lender is still getting their interest payments

– Now can have two entities on the hook for payments per their contractual arrangement.

Cons:

– They are not capturing the new higher rate as a lender.

So Should A Home Buyer Go Back in Time?

This is a question that can only be answered by a home buyer making the decision and their real estate attorney (If I did an assumable mortgage I would have my real estate attorney take a look at the agreement and contract). Assuming a mortgage based on the data out there is a more complex way of acquiring a home, but in the long run based on the interest environment and home inventory could be a good way to get into the real estate market.