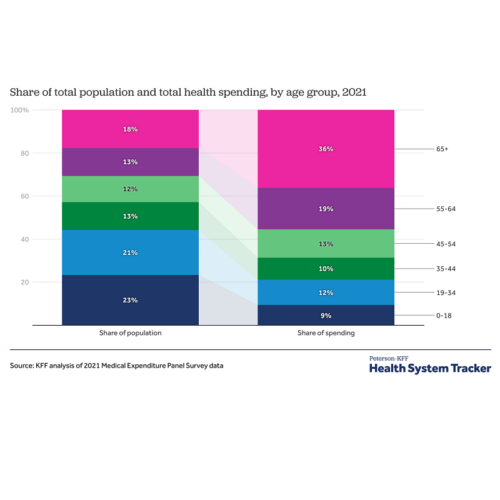

Are you more likely to spend more on medical expenses at age 26 or 66? For most people the answer is simple, more is spent on healthcare in retirement years – and the data backs it up. A 2021 study shows that the 65+ population spent 3x the amount of the 19-34 age group, despite being a smaller share of the population.

Young, employed, healthy people should consider using the triple magic of a health savings account (HSA) to save and invest for this period in life – with a huge tax advantage.

(As with anything tax and health related – your specific situation may vary, and you should consult a tax accountant before making any tax related investment decisions.)

Quick refresher on what an HSA is:

· A Health Savings Account (HSA) is a tax-advantaged savings account that helps save for medical expenses.

· To open an HSA, you must have a high-deductible health plan (HDHP) at work. These plans have higher deductibles (minimum spends before the insurance plan kicks in) and lower premiums (what you pay monthly) compared to traditional health plans.

· HSAs are owned by you, so the account remains yours through a job change. Money in HSAs roll over from year to year, allowing the balance to grow over time.

Ok cool, so what’s so different from this and a savings account? Let’s start with the triple tax magic.

- Pre-Tax contributions: You contribute directly from a payroll deduction, which means you pay less in taxes each paycheck.

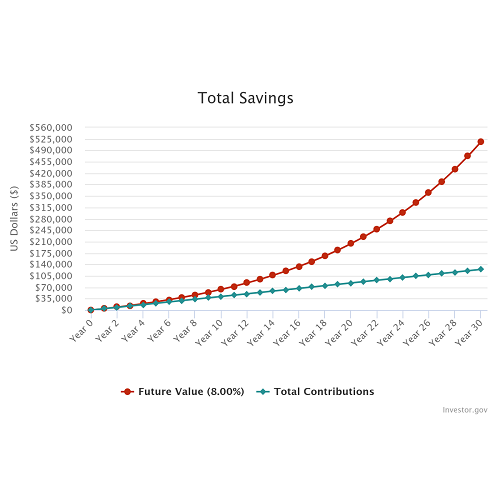

- Tax-Free Growth: The funds in the HSA can grow tax-free. How? HSA providers allow you to invest funds over a certain minimum into a range of mutual funds, ETF’s, Bonds, etc. For example: I have every dollar over $1,000 automatically invested into a low-fee Vanguard mutual fund which has historically grown at 8% per year.

- Tax-Free Withdrawals: You get a debit card with the account, and qualified medical expenses are tax-free, no matter your age. There’s a whole list of things you can buy with HSA dollars.

That’s impressive enough, but It could get even better – your employer may contribute. Some employers (including mine) match a percentage of every dollar contributed. Literally free money. There are annual contribution limits set by the IRS – $4,150 in 2024.

Let’s do some quick math: A 30-year-old today contributing the current HSA max $4,150/year until retiring at 65 would contribute $124,500. Assuming an 8% return over that time, your account would be worth over $500k at retirement, all tax free!! An incredible way to save for a category of expense that is likely to greatly increase over time.